Bookkeeping

Closing Entries Accounting Examples Beginners:Step by Step

Closing journal entries are used at the end of the accounting cycle to close the temporary accounts for the accounting period, and transfer the balances to the retained earnings account. Closing entries are posted in the general ledger by transferring all revenue and expense account balances to the income summary account. Then, transfer the balance of the income summary account to the retained earnings account. In short, we can clear all temporary accounts to retained earnings with a single closing entry. By debiting the revenue account and crediting the dividend and expense accounts, the balance of $3,450,000 is credited to retained earnings. Companies use closing entries to reset the balances of temporary accounts − accounts that show balances over a single accounting period − to zero.

Should closing entries be performed before or after adjusting entries?

We can also see that the debit equals credit; hence, it adheres to the accounting principle of double-entry accounting. After this closing entry has been posted, each of these revenue accounts has a zero balance, whereas the Income Summary has a credit balance of $7,400. After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal account will now also be zero. At the end of a financial period, businesses will go through the process of detailing their revenue and expenses. The closing journal entries example comprises of opening and closing balances.

- He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries.

- Once adjusting entries have been made, closing entries are used to reset temporary accounts.

- If it does, you’ll need to debit retained earnings and credit dividends like in the example here.

- As well as being consistently up-to-date on the financial health of your business.

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR

Remember that expense accounts have a normal debit balance so a credit will zero out their balance and then you can debit the income summary to move it. Remember that revenue accounts normally have a credit balance so here we are debiting them to zero them out. Dividend account is credited to record the closing entry for dividends. The $1,000 net profit balance generated through the accounting period then shifts.

Great! The Financial Professional Will Get Back To You Soon.

Remember that all revenue, sales, income, and gain accounts are closed in this entry. Lastly, you’ll repeat the process for each temporary account that you have to close. Alright, with a high-level understanding let’s dive into the 4-step close process. They are special entries posted at the end of an accounting period. Using the above steps, let’s go through an example of what the closing entry process may look like. We’ll use a company called MacroAuto that creates and installs specialized exhaust systems for race cars.

Let’s Recap Accounting Closing Entries:

The retained earnings account is reduced by the amount paid out in dividends through a debit and the dividends expense is credited. Income summary is a holding account used to aggregate all income accounts what is the weighted average contribution margin in break except for dividend expenses. It's not reported on any financial statements because it's only used during the closing process and the account balance is zero at the end of the closing process.

Accounting made for beginners

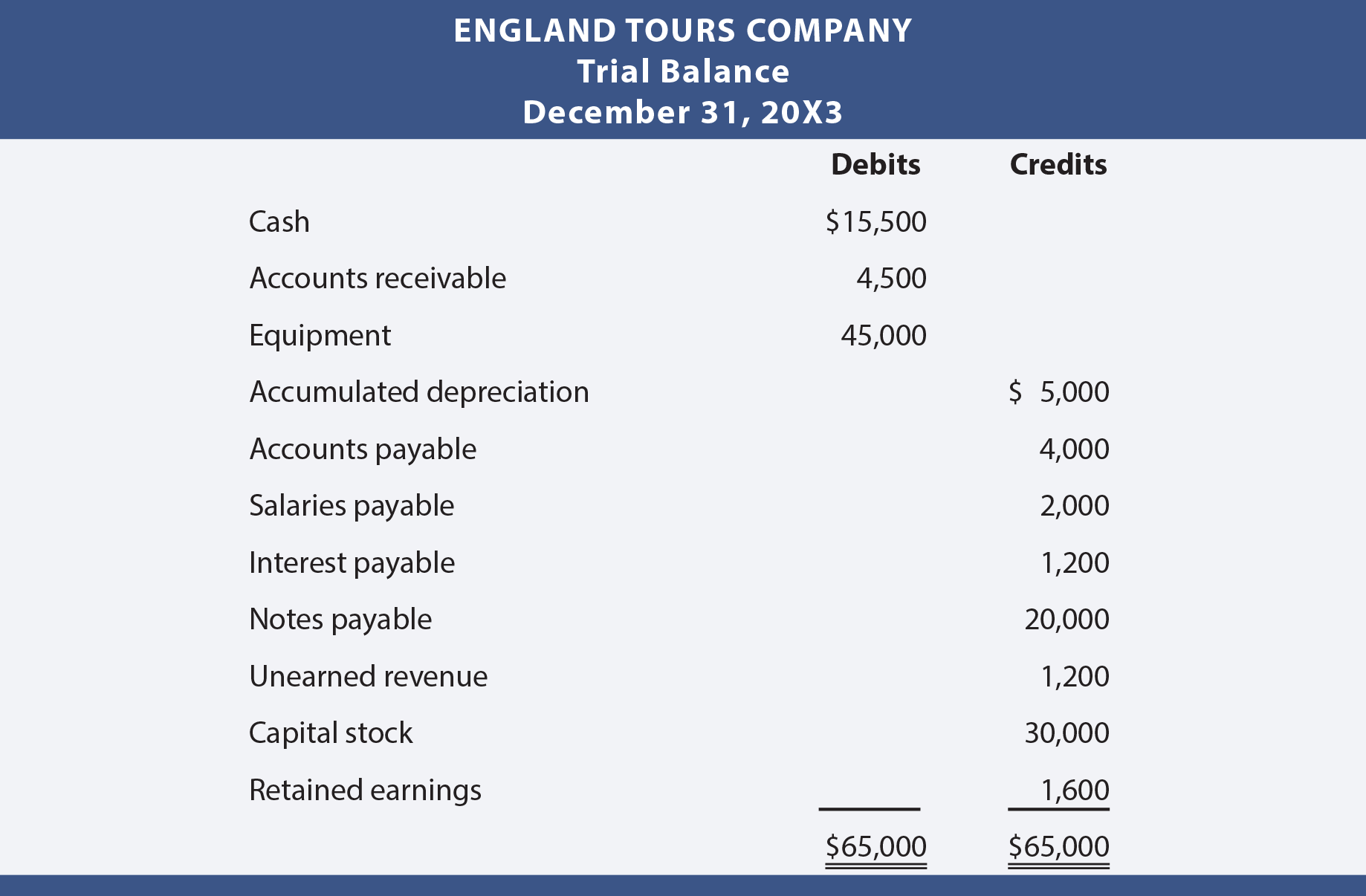

As we mentioned, these include revenue, expense, and dividend accounts. From this trial balance, as we learned in the prior section, you make your financial statements. After the financial statements are finalized and you are 100 percent sure that all the adjustments are posted and everything is in balance, you create and post the closing entries. The closing entries are the last journal entries that get posted to the ledger. After the posting of this closing entry, the income summary now has a credit balance of $14,750 ($70,400 credit posted minus the $55,650 debit posted).

Although the drawings account is not an income statement account, it is still classified as a temporary account and needs a closing journal entry to zero the balance for the next accounting period. Closing entries are performed after adjusting entries in the accounting cycle. Adjusting entries ensures that revenues and expenses are appropriately recognized in the correct accounting period. Once adjusting entries have been made, closing entries are used to reset temporary accounts. Closing entries are journal entries made at the end of an accounting period, that transfer temporary account balances into a permanent account. Now that all the temporary accounts are closed, the income summary account should have a balance equal to the net income shown on Paul’s income statement.

Now Paul must close the income summary account to retained earnings in the next step of the closing entries. Lastly, prepare a post-closing trial balance to verify that the balances of the permanent accounts are correct and that the temporary accounts have been reset to zero. Although it is not an income statement account, the dividend account is also a temporary account and needs a closing journal entry to zero the balance for the next accounting period.

The closing entry entails debiting income summary and crediting retained earnings when a company’s revenues are greater than its expenses. The income summary account must be credited and retained earnings reduced through a debit in the event of a loss for the period. The income summary is used to transfer the balances of temporary accounts to retained earnings, which is a permanent account on the balance sheet.

Closing entries, on the other hand, are entries that close temporary ledger accounts and transfer their balances to permanent accounts. Temporary account balances can be shifted directly to the retained earnings account or an intermediate account known as the income summary account. Closing all temporary accounts to the income summary account leaves an audit trail for accountants to follow.

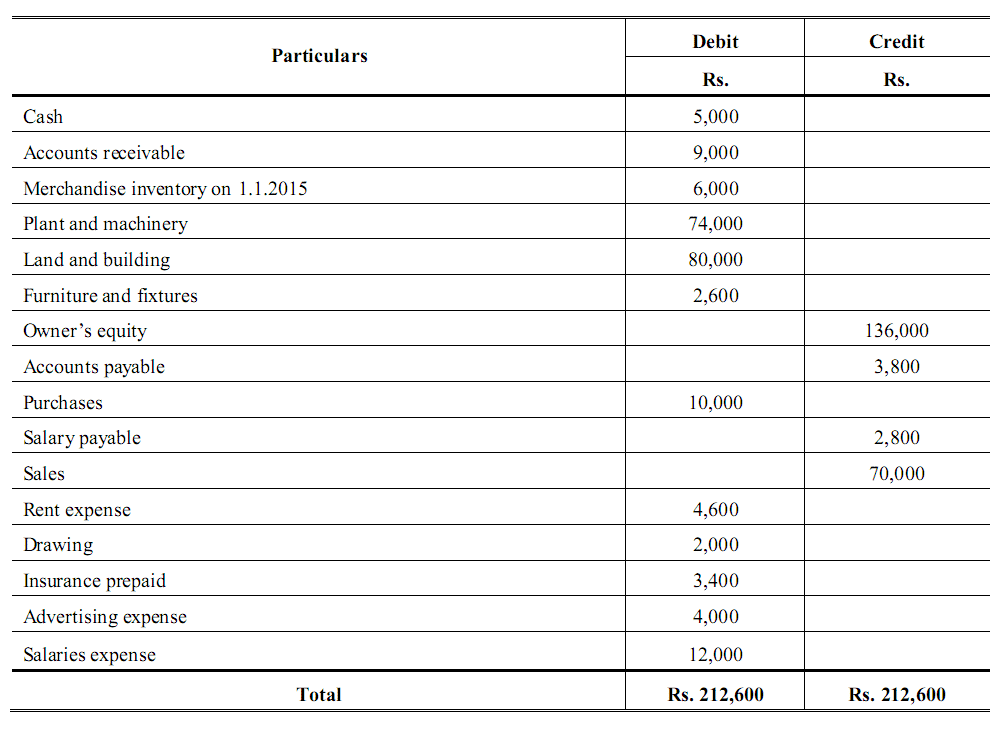

As you will see later, Income Summary is eventually closed to capital. The following example shows the closing entries based on the adjusted trial balance of Company A. Any remaining balances will now be transferred and a post-closing trial balance will be reviewed. Closing entries are the journal entries used at the end of an accounting period.